In every modern democracy, the State requires financial resources to function effectively. Governments build roads, maintain public infrastructure, provide healthcare, support education, strengthen national security, administer justice, and implement welfare programs—all of which require substantial revenue. However, an important constitutional question arises: Where does the State derive its authority to collect money from citizens?

The answer lies in the Constitution.

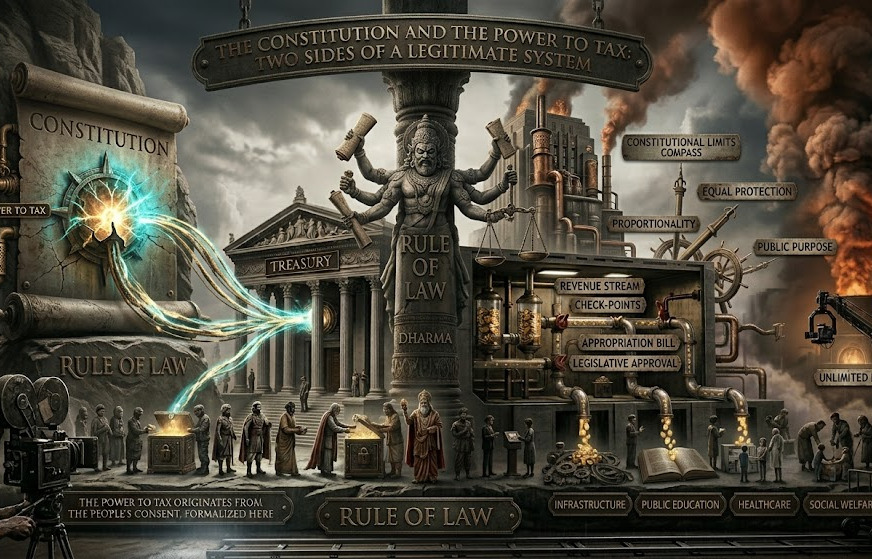

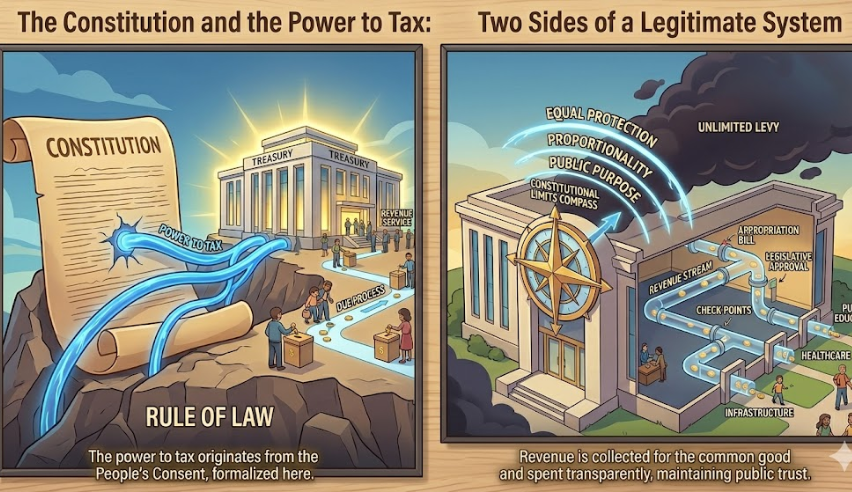

The Constitution acts as a strict legal framework that not only authorizes the State to collect revenue but also places limits on that authority to prevent abuse. It serves as the foundation upon which taxation, public finance, and fiscal governance are built. Without constitutional authorization, any attempt by the State to collect money from citizens would be arbitrary, unlawful, and incompatible with democratic principles.

This article explores how the Constitution legalizes, limits, and legitimizes the State’s power to collect revenue while safeguarding the rights of citizens.

Understanding State Revenue

State revenue refers to all financial resources collected by the government to fund public administration and developmental activities.

These revenues generally come from:

- Taxes

- Duties

- Fees

- Cesses

- Fines and penalties

- Borrowings

- Public sector earnings

- Grants and transfers

Among these sources, taxation remains the most significant and consistent source of government income.

Yet taxation is unique because it involves compulsory extraction of money from citizens. Unlike a commercial transaction, taxpayers do not voluntarily choose whether to pay taxes. Therefore, democratic societies require a constitutional basis for such coercive power.

This is where constitutional law becomes indispensable.

Why Governments Cannot Tax Without Constitutional Authority

One of the most fundamental principles of constitutional governance is that government power is not unlimited.

In monarchies and authoritarian systems, rulers historically imposed taxes according to their discretion. Such practices often led to oppression, economic exploitation, and public unrest.

The emergence of constitutional democracies changed this paradigm by establishing a simple yet powerful principle:

The government can only exercise powers granted by law.

Taxation, being a significant intrusion into private property and individual wealth, requires explicit legal authorization.

The Constitution therefore acts as the ultimate source of legitimacy for every taxation measure adopted by the State.

Without constitutional authority:

- Tax collection becomes arbitrary.

- Citizens lose protection against excessive taxation.

- Government actions become vulnerable to abuse.

- Rule of law is undermined.

Thus, constitutional authorization transforms taxation from an act of force into an act of lawful governance.

Constitutional Legalization of Revenue Collection

The Constitution legalizes the State’s power to collect revenue by expressly granting taxing powers to governmental institutions.

In India, the Constitution carefully distributes fiscal authority between the Union Government and State Governments.

This allocation ensures:

- Fiscal balance

- Administrative efficiency

- Federal harmony

- Prevention of jurisdictional conflicts

The Constitution specifies:

- Which level of government may impose particular taxes.

- How revenue shall be shared.

- How financial relations between governments shall operate.

This constitutional framework prevents confusion and creates predictability in revenue administration.

The authority to impose taxes therefore does not originate from political convenience but from constitutional design.

Article 265: The Constitutional Shield Against Arbitrary Taxation

One of the most important safeguards in the Indian Constitution is Article 265, which states:

“No tax shall be levied or collected except by authority of law.”

This provision serves as a constitutional barrier against arbitrary fiscal action.

The Article contains two critical requirements:

Levy Must Be Authorized by Law

Before a tax can exist, a competent legislature must enact a law authorizing it.

The executive cannot independently create taxes.

Collection Must Be Lawful

Even after a tax is imposed, its collection must strictly follow legal procedures.

Government authorities cannot collect taxes outside the framework established by law.

Article 265 therefore protects citizens from unlawful financial burdens while ensuring governmental accountability.

Constitutional Limits on Revenue Collection

The Constitution does not merely grant power—it also restricts power.

This dual function is essential to constitutional governance.

A government that possesses unrestricted taxing authority could potentially:

- Confiscate wealth.

- Suppress economic activity.

- Discriminate against specific groups.

- Violate fundamental rights.

To prevent such outcomes, constitutional systems impose legal limitations.

These limitations include:

Legislative Competence

Only the appropriate legislature may enact a tax.

A tax imposed by an authority lacking constitutional competence may be declared invalid.

Fundamental Rights Protection

Revenue laws must respect constitutional rights.

Taxation measures cannot violate principles such as:

- Equality before law

- Non-discrimination

- Due process

- Freedom of trade and profession

Courts may strike down taxation provisions that infringe constitutional guarantees.

Judicial Review

The judiciary serves as the guardian of constitutional limits.

Courts possess the authority to examine:

- Whether a tax is constitutionally valid.

- Whether proper legislative procedures were followed.

- Whether constitutional rights have been violated.

This judicial oversight strengthens accountability and protects taxpayers.

Constitutional Legitimacy and Public Trust

Revenue collection is not merely a legal issue—it is also a question of legitimacy.

Citizens are more likely to comply with tax obligations when they perceive the taxation system as:

- Fair

- Transparent

- Lawful

- Accountable

The Constitution provides this legitimacy.

When taxes are imposed according to constitutional procedures, citizens recognize them as expressions of democratic governance rather than governmental coercion.

Constitutional legitimacy transforms taxation from a burden imposed by rulers into a civic responsibility shared by members of a democratic society.

Constitutionalism and Fiscal Responsibility

Constitutional governance requires governments to exercise fiscal powers responsibly.

The Constitution encourages:

- Financial transparency

- Budgetary accountability

- Legislative oversight

- Responsible expenditure

Public funds collected through taxation must ultimately serve public purposes.

Governments are therefore expected to justify both:

- Why revenue is collected.

- How revenue is spent.

This principle reinforces democratic accountability and strengthens citizen confidence in public institutions.

Federalism and Revenue Distribution

India’s Constitution establishes a federal system in which financial powers are divided between different levels of government.

The Constitution determines:

- Revenue assignments.

- Tax-sharing arrangements.

- Grants-in-aid mechanisms.

- Financial transfers.

This framework prevents excessive concentration of fiscal power and promotes cooperative federalism.

Through institutions such as the Finance Commission, constitutional mechanisms ensure equitable distribution of resources across states.

As a result, constitutional fiscal arrangements contribute to balanced regional development and national unity.

Revenue Collection and the Rule of Law

The rule of law is one of the most important constitutional principles governing taxation.

Under the rule of law:

- Government actions must be legally authorized.

- Public officials remain accountable.

- Citizens receive equal treatment.

- Arbitrary power is prohibited.

Revenue collection conducted under constitutional authority strengthens the rule of law because it subjects governmental financial power to legal control.

Every assessment, demand, and collection action must ultimately trace its legitimacy back to constitutional principles.

The Social Contract Behind Taxation

Taxation is often understood through the concept of the social contract.

Citizens contribute a portion of their income and wealth to the State.

In return, the State provides:

- Security

- Infrastructure

- Public services

- Welfare measures

- Economic development

The Constitution acts as the written expression of this social contract.

It establishes the conditions under which citizens surrender part of their resources and defines the obligations of government in return.

Thus, constitutional taxation reflects a balance between individual rights and collective welfare.

Challenges in Modern Revenue Governance

Modern governments face increasingly complex fiscal challenges.

These include:

- Digital economy taxation

- Cross-border transactions

- Cryptocurrency regulation

- Tax avoidance strategies

- Globalization of commerce

- Expanding welfare obligations

Despite these evolving challenges, constitutional principles remain constant.

Every new taxation measure must continue to satisfy the requirements of:

- Legality

- Fairness

- Competence

- Accountability

- Constitutional validity

The Constitution therefore remains the enduring foundation of modern fiscal governance.

Conclusion

The Constitution is far more than a political document—it is the legal foundation of the State’s financial authority. It legalizes the government’s power to collect revenue, limits that power through constitutional safeguards, and legitimizes taxation through democratic consent and the rule of law.

Without constitutional authorization, taxation would amount to arbitrary state action. With constitutional authorization, taxation becomes a lawful instrument for public welfare, national development, and democratic governance.

In essence, the Constitution performs three indispensable functions in relation to state revenue: