Introduction

Taxation is the lifeblood of any modern state. Governments require revenue to provide public services, build infrastructure, maintain law and order, and ensure economic development. However, the power to tax is also one of the most significant powers a government possesses. Without constitutional limitations, taxation could easily become arbitrary, excessive, or discriminatory.

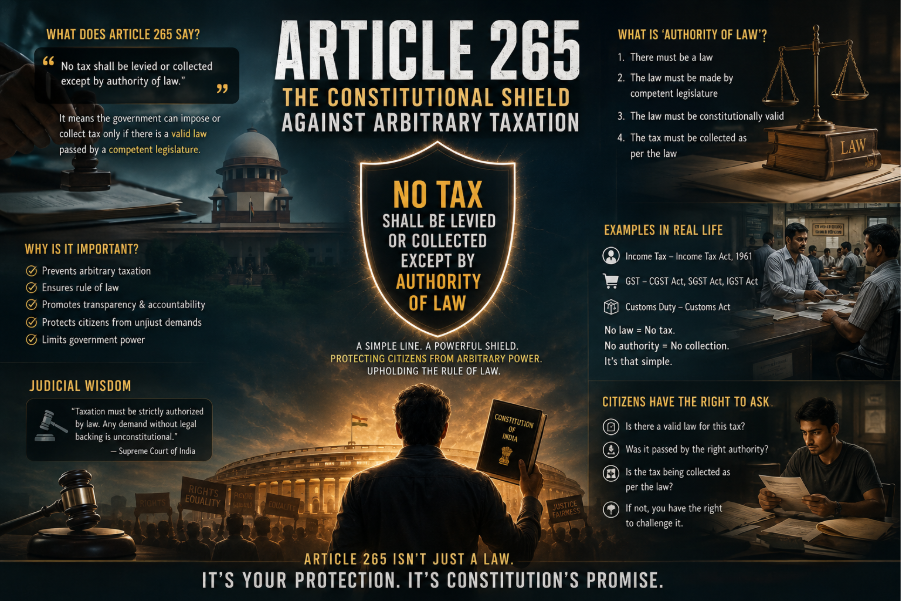

Recognizing this danger, the framers of the Indian Constitution incorporated a powerful safeguard in Article 265, which states:

“No tax shall be levied or collected except by authority of law.”

Though seemingly simple, this provision serves as a cornerstone of India’s constitutional and fiscal framework. It ensures that citizens are protected from unauthorized taxation and that the government’s revenue-raising powers remain subject to the rule of law.

Understanding Article 265

Article 265 is located in Part XII of the Constitution of India, which deals with Finance, Property, Contracts, and Suits. The provision establishes a fundamental constitutional principle:

The government cannot impose, collect, or retain a tax unless it is backed by a valid law enacted by a competent legislative authority.

This means that taxation cannot be based on:

- Administrative orders

- Executive instructions

- Government circulars

- Departmental notifications without statutory backing

- Arbitrary decisions of public officials

Only a duly enacted law passed by the appropriate legislature can authorize taxation.

The Meaning of “Authority of Law”

The phrase “authority of law” is the heart of Article 265.

For a tax to be constitutionally valid, the following conditions must be satisfied:

1. Existence of a Law

There must be a specific statute authorizing the levy and collection of tax.

For example:

- Income Tax is collected under the Income-tax Act, 1961.

- GST is collected under the CGST Act, 2017, SGST Acts, and IGST Act, 2017.

- Customs duties are imposed under the Customs Act and Customs Tariff Act.

Without legislative authority, tax collection becomes unconstitutional.

2. Competent Legislature

The law must be enacted by a legislature having constitutional power over that subject.

India follows a federal structure where taxation powers are divided between:

- Parliament

- State Legislatures

A state cannot impose a tax reserved exclusively for Parliament, and vice versa.

3. Constitutional Validity

Even if a law exists, it must comply with constitutional provisions.

A tax law violating:

- Fundamental Rights

- Federal distribution of powers

- Constitutional limitations

may be struck down by courts.

Why Article 265 Matters

Protection Against Arbitrary Government Action

Article 265 prevents governments from raising revenue through executive whims.

Imagine a situation where a government department suddenly demands a new fee or tax without legislative approval. Article 265 empowers citizens to challenge such demands before the courts.

This safeguard ensures that public authorities remain accountable and operate within constitutional boundaries.

Strengthening the Rule of Law

The rule of law requires that all government actions be authorized by law.

Article 265 reinforces this principle by ensuring that taxation is not based on discretion but on democratically enacted legislation.

Citizens are therefore taxed not by individual officials but by laws passed through representative institutions.

Promoting Transparency and Accountability

Since taxes must originate from legislation, taxpayers gain access to:

- Clear legal provisions

- Defined tax rates

- Prescribed procedures

- Available remedies and appeals

This transparency creates trust between taxpayers and the government.

Judicial Interpretation of Article 265

Indian courts have consistently treated Article 265 as a strong constitutional safeguard.

Kunnathat Thathunni Moopil Nair v. State of Kerala (1961)

The Supreme Court emphasized that taxation laws must comply with constitutional principles and cannot operate arbitrarily.

The judgment highlighted that taxing powers are not unlimited and remain subject to constitutional scrutiny.

Commissioner of Income Tax v. Eli Lilly & Co.

The Court reaffirmed that tax collection must strictly conform to statutory authority.

Even genuine government revenue interests cannot justify collection beyond legal authorization.

Principle Established by Courts

The judiciary has repeatedly held:

If a tax lacks statutory authority, the government has no constitutional right to collect it.

Similarly, taxes collected without legal backing may have to be refunded.

Article 265 and the GST Era

The introduction of the Goods and Services Tax (GST) in 2017 transformed India’s indirect tax system.

Even under GST, Article 265 remains highly relevant.

Every GST demand must be supported by:

- Constitutional authority

- Legislative enactment

- Proper procedural compliance

Tax authorities cannot create liabilities merely through departmental circulars or administrative interpretations.

Any demand inconsistent with the law can be challenged using constitutional principles derived from Article 265.

Difference Between Tax and Fee

Article 265 primarily governs taxation.

A tax generally involves:

- Compulsory extraction of money

- No direct benefit to the payer

- Revenue for public purposes

A fee, on the other hand, is usually linked to a specific service provided by the government.

However, courts often examine whether a levy labeled as a “fee” is actually a disguised tax. If so, constitutional requirements under Article 265 become applicable.

The Citizen’s Constitutional Protection

For ordinary citizens and businesses, Article 265 acts as a constitutional shield.

Whenever a tax demand is raised, the following questions can be asked:

- Is there a valid law authorizing this tax?

- Was the law enacted by a competent legislature?

- Is the law constitutionally valid?

- Has the tax been collected according to statutory procedures?

If the answer to any of these questions is negative, the levy may be challenged before the courts.

Relevance in Modern Governance

As governments increasingly rely on digital taxation, GST compliance systems, and evolving revenue mechanisms, constitutional safeguards become even more important.

Article 265 ensures that:

- Technology does not replace legality.

- Administrative convenience does not override constitutional authority.

- Revenue collection remains subject to democratic control.

In an era of expanding fiscal powers, Article 265 continues to preserve the balance between state authority and citizen rights.

Conclusion

Article 265 may consist of only a few words, but its constitutional significance is immense. It embodies the principle that taxation must never be arbitrary and that every rupee collected by the government must have legal sanction.

By requiring the authority of law for every tax levy and collection, Article 265 protects citizens from unauthorized financial burdens, strengthens democratic accountability, and reinforces the rule of law.

In essence, Article 265 is not merely a fiscal provision—it is a constitutional guarantee that government power over taxation will always remain subordinate to law, justice, and constitutional governance.