Introduction

When passengers book an airline ticket, the final amount paid often differs significantly from the advertised base fare. Taxes, airport charges, convenience fees, and regulatory levies contribute to the total cost of air travel.

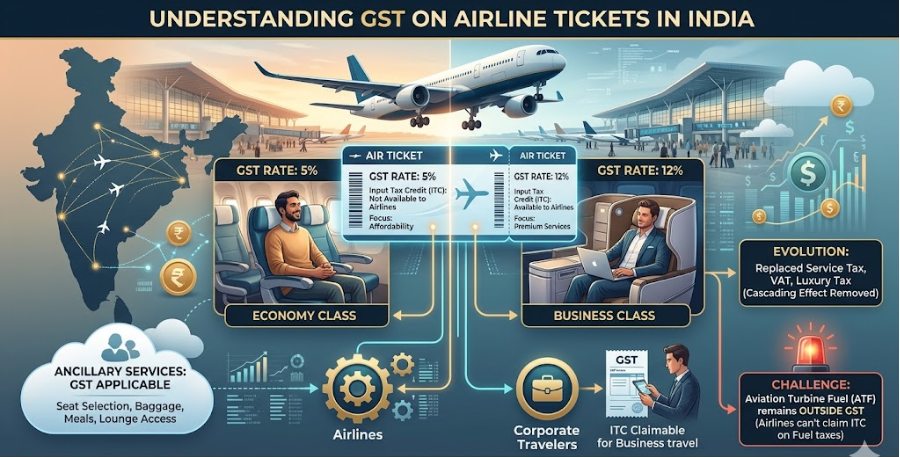

Among these components, the Goods and Services Tax (GST) plays a crucial role in determining ticket prices in India. Introduced in July 2017, GST transformed the indirect taxation landscape by replacing multiple taxes with a unified framework.

For airlines, travel agencies, and passengers, understanding GST is essential—not only for cost transparency but also for compliance, input tax credit claims, and business travel expense management.

This article explores how GST applies to airline tickets, its impact on consumers and businesses, and the challenges and opportunities it creates for the aviation sector.

The Evolution of Indirect Taxation in Aviation

Before GST, airline tickets in India were subject to various indirect taxes, including:

- Service Tax

- Value Added Tax (VAT) on aviation turbine fuel

- Luxury taxes in certain jurisdictions

- Airport-related charges and cesses

The fragmented tax structure created operational complexities for airlines and increased compliance burdens.

The implementation of GST aimed to:

- Simplify tax administration

- Eliminate cascading taxes

- Improve transparency

- Enhance ease of doing business

- Enable seamless input tax credits

While GST streamlined several aspects of aviation taxation, certain areas—such as aviation turbine fuel (ATF)—remain outside the GST regime, limiting the industry’s ability to fully optimize costs.

GST Rates Applicable to Airline Tickets

GST rates on airline tickets depend primarily on the class of travel.

Economy Class

- GST Rate: 5%

- Input Tax Credit (ITC): Not available to airlines on input services used for supplying economy class tickets

Business Class

- GST Rate: 12%

- Input Tax Credit (ITC): Available to airlines

The distinction aims to keep economy travel affordable while allowing airlines to recover taxes on higher-value premium services.

Illustrative Example

Assume the base fare for a domestic journey is ₹10,000.

Economy Class

- Base Fare: ₹10,000

- GST @ 5%: ₹500

- Total: ₹10,500 (excluding airport charges and convenience fees)

Business Class

- Base Fare: ₹10,000

- GST @ 12%: ₹1,200

- Total: ₹11,200 (excluding additional charges)

Passengers should note that GST applies only to specific fare components and not necessarily to the entire ticket amount.

GST on Domestic vs. International Air Travel

GST treatment varies depending on the nature of travel.

Domestic Flights

Flights operating entirely within India attract GST according to the applicable class of service.

Examples:

- Hyderabad to Delhi

- Mumbai to Bengaluru

- Chennai to Kolkata

GST is charged directly on the airfare.

International Flights

International air transportation is generally treated as an export of services under the GST framework.

As a result:

- GST may not apply to the international leg of the journey.

- Certain booking components may still attract taxes.

- Ancillary services may be taxed separately.

For itineraries involving both domestic and international sectors, GST applicability depends on the place of supply rules and ticket structure.

Travelers should carefully review their ticket breakdown to understand applicable taxes.

GST on Ancillary Airline Services

Modern airline revenue extends beyond ticket sales.

Additional services often include:

- Seat selection

- Priority boarding

- Extra baggage allowance

- Lounge access

- In-flight meals

- Rescheduling charges

- Cancellation fees

These ancillary services generally attract GST at applicable rates based on their classification.

For example:

| Service | Typical GST Treatment |

| Extra baggage | GST applicable |

| Seat selection | GST applicable |

| Cancellation fee | GST applicable |

| Convenience fee | GST applicable |

| Lounge access | GST applicable |

Passengers should remember that the GST shown on the final invoice may include taxes on these add-on services.

Input Tax Credit and Corporate Travel

Input Tax Credit (ITC) is one of the most significant features of the GST framework.

Businesses booking air travel for official purposes may be eligible to claim ITC, subject to certain conditions.

Conditions for Claiming ITC

- Travel must be for business purposes.

- The GST invoice must contain the company’s GSTIN.

- The expense must not fall under blocked credit provisions.

- The supplier must have deposited the tax with the government.

- The transaction must appear in GST returns.

Benefits for Businesses

- Reduced effective travel costs

- Improved tax efficiency

- Better expense management

- Enhanced transparency in procurement

Companies with significant travel budgets can realize substantial savings through proper GST compliance and documentation.

Impact of GST on Airlines

GST has had both positive and negative implications for the aviation sector.

Positive Outcomes

Simplified Tax Structure

Airlines no longer deal with multiple indirect taxes across jurisdictions.

Improved Compliance Systems

Digitized tax reporting has enhanced transparency.

Better Input Tax Management

Business class operations benefit from input tax credits.

Enhanced Audit Trails

GST has strengthened financial accountability and documentation.

Persistent Challenges

Aviation Turbine Fuel Remains Outside GST

ATF accounts for a substantial portion of airline operating costs.

Since ATF is taxed under state VAT regimes:

- Airlines cannot claim input tax credits on fuel taxes.

- Operational costs remain high.

- Tax inefficiencies continue.

Industry stakeholders have consistently advocated for bringing ATF under GST.

Complex Fare Structures

Different GST rates for various services create compliance challenges.

Frequent Regulatory Updates

Airlines and travel intermediaries must continuously adapt to changing tax rules and interpretations.

GST and Online Travel Agencies (OTAs)

Online travel agencies have transformed ticket distribution.

Major revenue streams for OTAs include:

- Convenience fees

- Service charges

- Commission income

- Advertising partnerships

GST implications differ based on the business model.

Key considerations include:

- Place of supply rules

- Cross-border transactions

- Commission structures

- Invoice generation

- Input tax credit reconciliation

For travel agencies, maintaining robust compliance systems is critical to avoiding disputes and penalties.

Passenger Awareness: Reading Your Ticket Correctly

Many travelers focus only on the final ticket price without understanding its components.

A typical airline ticket may include:

- Base fare

- GST

- User Development Fee (UDF)

- Passenger Service Fee (PSF)

- Airport charges

- Convenience fee

- Fuel surcharge

- Ancillary service charges

Understanding these components helps passengers:

- Compare fares effectively

- Identify refundable elements

- Verify GST charges

- Claim business travel expenses accurately

Always request a GST-compliant invoice if you intend to claim input tax credit.

The Future of GST in Indian Aviation

As India’s aviation market continues to expand, policymakers are expected to revisit several taxation issues.

Potential reforms may include:

- Inclusion of aviation turbine fuel under GST

- Rationalization of GST rates

- Simplification of place-of-supply rules

- Digitization of tax compliance systems

- Standardization of ancillary service taxation

Such reforms could reduce operating costs, improve airline profitability, and make air travel more affordable.

India is projected to become one of the world’s largest aviation markets, making tax efficiency a critical factor in sustaining long-term growth.

Conclusion

GST has significantly reshaped the taxation framework for airline tickets in India.

While the dual-rate structure seeks to balance affordability and revenue generation, challenges remain—particularly regarding aviation turbine fuel and the complexity of ancillary services.

For passengers, understanding GST enables informed travel decisions and accurate expense management.

For businesses, effective GST compliance unlocks valuable input tax credits.

For airlines, future tax reforms could play a decisive role in improving operational efficiency and competitiveness.

As the aviation ecosystem evolves, a transparent, simplified, and technology-driven GST framework will be essential to supporting India’s ambition of becoming a global aviation powerhouse.

Key Takeaways

- Economy class tickets attract GST at 5%.

- Business class tickets attract GST at 12%.

- Input tax credit is generally available for business class travel.

- Ancillary airline services often attract separate GST charges.

- Corporate travelers should ensure GST-compliant invoicing.

- Aviation turbine fuel remains outside the GST framework.

- Future reforms could significantly reduce airline operating costs.